As Oil Supply Tightens and War Continues, Is the Petrodollar Era Ending.

|

| Image:Watcher Guru |

Petroyuan use in Hormuz is anecdotal but tied to current war. A Fortune article (April 7, 2026) reports Saudi Arabia "quietly killed the petrodollar two years ago" (i.e., ~2024), ending the exclusive USD-for-oil agreement originally struck in 1974. This aligns with prior diversification: since the 1980s, Saudi Arabia has led OPEC surpluses (42% share), but by 2022, it began talks with China to sell oil in e-yuan (not USD), despite U.S. pressure to maintain USD exclusivity (Taylor & Francis journal, 2026; citing Geopoliticaleconomy 2023a, He 2022).The U.S.-Israel war on Iran (ongoing as of March 18, 2026, per Capital Street FX) has accelerated this. Iran closed the Strait of Hormuz (20% of global oil trade), but some ships pass by paying in Chinese yuan. Gulf states have diversified oil trade away from USD for years, with economists noting the dollar's global reserve share fell from 71% (1999) to 57% (recent low) (EBC Financial Group analyst Michael Harris).These build on historical context: The 1974 U.S.-Saudi pact required oil sales in USD, with proceeds recycled into U.S. banks/Treasuries, but Saudi-China ties (China as top trading partner) and e-yuan pilots signal a "major shift" (2022 onward). U.S pressured Saudi Arabia (OPEC leader) to increase supply and lower prices to hurt Russia/Iran oil revenues amid regional turmoil (Iraq/Syria ISIS crisis). John Kerry allegedly dealt with King Abdullah for below-market sales, explaining price drops despite instability (Guardian via Elliott 2014, cited in journal). Medium—war exposes supply vulnerabilities (Strait closure), but decisions inferred from patterns, not direct 2026 announcements. Dollar dominance persists but is "no longer the only game" (Fortune). This could affect everything from your mortgage rate to the price of filling your tank

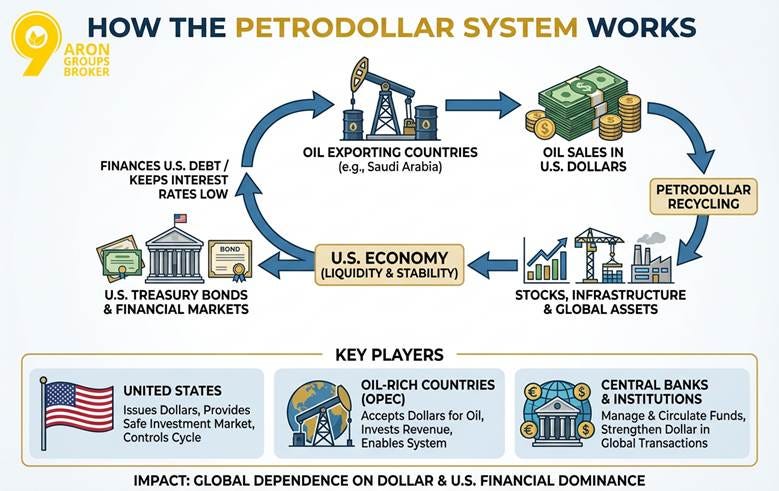

BACKGROUND OF THE PETRODOLLAR:

|

| image:Arie van Gemeren,CFA |

The petrodollar refers to the global practice of pricing and settling most oil trades in US dollars, originating from a 1974 US-Saudi Arabia agreement where Saudi Arabia agreed to price its oil exclusively in dollars in exchange for US military protection and access to American financial markets; other OPEC nations largely followed this convention after the 1971 collapse of the Bretton Woods gold standard.After President Nixon ended dollar-gold convertibility in 1971, the US sought to maintain dollar demand. In 1974, a deal with Saudi Arabia—often called the petrodollar agreement—required Saudi oil sales in dollars, with revenues recycled into US Treasuries; this was not a formal treaty but a pragmatic arrangement that spread to OPEC members, making dollars essential for oil imports worldwide due to oil's status as the top traded commodity. Pre-1970s, about 20% of oil traded in British pounds, but dollar dominance grew to over 94%, reinforced by network effects, deep US markets, and habit rather than legal mandate. Oil priced in dollars creates perpetual global demand for USD, as importers must acquire dollars, boosting liquidity for US deficits via "petrodollar recycling"—exporters invest surpluses in US Treasuries, financing low-cost US debt (over $35 trillion today) and stabilizing rates.This resolves the Triffin dilemma (reserve currency nations must run deficits for global liquidity), enhancing dollar reserve status through oil-backed trust, geopolitical leverage, and IMF standards reporting reserves in dollars; no other currency has this commodity anchor. Critics note it's more about surplus management than pricing alone, with liquid forex markets allowing euro settlements via dollar forwards. The dollar remains dominant due to liquidity, switching costs, and market depth, but faces erosion from de-dollarization: Russia, Saudi Arabia, Iran, Venezuela, and others accept yuan (petroyuan), euros, or barter in bilateral deals since 2018; BRICS pushes alternatives amid US sanctions and energy transitions to renewables. No full collapse dollar handles ~80-90% of trades—but strains grow from "weaponized" sanctions and green energy shifts reducing oil's role.

RISING CONCERNS AND POINTS:

|

| Image:Investing.com |

Sanctions and financial restrictions are pushing energy supply risks, with Saudi Arabia's energy minister warning they could lead to shortages alongside reduced investments. This incentivizes non-dollar settlements by heightening tensions, such as past U.S.-Saudi friction over OPEC+ production cuts, though there’s lack direct evidence of dollar avoidance; recent U.S.-Saudi pacts emphasize dollar-aligned cooperation like financial partnerships and critical minerals supply chains. Instead, ongoing U.S.-Saudi energy deals, including a bilateral dialogue on oil, gas, electricity, and nuclear power, a 2025 nuclear cooperation declaration positioning Saudi Arabia as a potential U.S. uranium supplier, and critical minerals frameworks for rare earths and uranium supply chains. coverage focuses on U.S.-Saudi strategic ties in energy and finance.

OPEC+ (led by Saudi Arabia "Saudi Arabia yuan currency" and including Russia) implemented voluntary production cuts of 2 million b/d in 2023, extended through 2026, amid U.S. tensions and recession fears, but has since accelerated unwinding these cuts (e.g., +411,000 b/d in May and June 2026) due to low inventories and healthy markets. U.S. sanctions on Russian oil target flows to China and India, potentially benefiting Saudi exports there, while Saudi production hikes aim to regain Asian market share despite price drops (e.g., U.S. benchmark fell to $61/bbl). Broader U.S. responses to Saudi-led cuts include options like easing sanctions on other producers or using the Strategic Petroleum Reserve, but recent Trump-era discussions prioritize arms deals and investments over curbing Saudi output. Unrelated tensions include U.S. threats of sanctions on green shipping allies and Trump pledges to reopen the Strait of Hormuz amid U.S.-Iran talks, which could ease any Gulf shipping constraints. How will these shifts couple with Dedollarization, BRICS currency, oil supply shortage , war impact on oil prices, China Saudi energy deal, OPEC supply cut, and (Petroyuan and Petrodollar) currency wars.

THE PETROYUAN SHIFT:

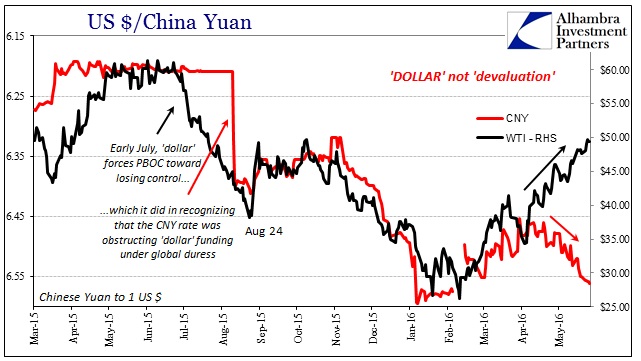

The "petroyuan" refers to the growing use of China's yuan (RMB) for pricing and settling oil and energy trades, challenging the long-dominant US "petrodollar" system. This shift gained momentum after Saudi Arabia ended its exclusive dollar-denominated oil sales agreement in June 2024, opening the door to yuan and other currencies.A petroyuan rise could weaken US financial dominance by reducing global demand for dollars and US Treasury bonds, historically sustained by petrodollar recycling (where oil exporters buy US debt).

|

| OIL PRICE HISTORY(IMAGE:THE CONVERSATION) |

Higher Borrowing Costs and Debt Pressure: The petrodollar ensured demand for US Treasuries, financing deficits at low rates. Its erosion could raise interest rates economy-wide, affecting mortgages and investments, while a weaker dollar fuels inflation via pricier imports.

Currency Weakness and Inflation: Less dollar demand in energy trade may devalue the USD, increasing import costs and domestic inflation.

Geopolitical Erosion: Conflicts like the Iran war could accelerate this, pushing Gulf states toward Asia and yuan pricing, undermining dollar usage in trade and reserves .Sources note the dollar still leads (39% of payments vs. yuan's 28%) but warn of accelerating decline.Sources note the dollar still leads (39% of payments vs. yuan's 28%) but warn of accelerating decline. Consumers, especially in oil-importing nations, face mixed effects from currency diversification and volatility, though long-term benefits could emerge in a multipolar system.

Increased Volatility and Higher Energy Prices: Oil priced in multiple currencies (e.g., yuan baskets) could spike short-term volatility, raising gasoline and energy costs globally as markets adjust.

Inflationary Pressures: In the US, a weaker dollar means costlier imported oil/energy, hitting household budgets . Non-Western consumers might benefit from yuan stability in Asia-centric trade.

Potential Long-Term Savings: Yuan-denominated trade could lower transaction costs for China-linked economies, indirectly stabilizing prices if CBDCs streamline payments

Impacts vary: Western consumers may see short-term pain, while BRICS-aligned ones gain alternatives to dollar fluctuations

Implications for the Global Economy

The shift signals a move toward multipolar finance, with de-dollarization but no immediate yuan dominance due to capital controls and convertibility limits.

- Dollar Dominance Persists, USD retains edge via deep markets and trust. Stable trade; minimal disruption.

- Multi-Currency Coexistence, Petroyuan, petroeuro rise alongside dollar. Diversified reserves; reduced US leverage.

- Fragmented Trade, West uses dollars; East (China/Russia) uses yuan. Geopolitical blocs; higher hedging costs.

- Digital Currency Rise, CBDCs/blockchain for energy payments. Faster, cheaper trades; de-dollarization accelerates.

Sources depict a gradual transition , with petroyuan traction from China's import dominance (world's top energy buyer) and deals with Russia, Iran, Saudi Arabia. Full displacement is unlikely soon due to yuan barriers, but it challenges US "exorbitant privilege"

WHY PETROYUAN SHIFT IS STILL LONGTERM DISCUSSION:

The Chinese yuan (RMB) cannot fully replace the US dollar (USD) as the dominant global reserve currency primarily due to China's strict capital controls, insufficient market liquidity and depth, and rule of law concerns stemming from centralized political control and lack of transparency.

Capital Controls: China's capital controls restrict free inflows and outflows of money, preventing investors from easily buying, selling, or divesting RMB-denominated assets without government approval. This creates liquidity risks, as outflow controls can "lock in" foreign capital during crises, deterring central banks and investors who prioritize convertibility. The People's Bank of China (PBOC) uses these controls to manage the RMB's exchange rate tightly, prioritizing stability over internationalization, a policy that has tightened since 2023.

Liquidity and Market Depth: USD markets offer 24/7 trading, massive asset volumes, and minimal price disruption for large transactions, supporting global trade needs. RMB markets lack this depth and liquidity, with trading flows far smaller and limited outside China. As of recent data, RMB holds only 2.5-2.7% of global reserves versus USD's 58-66%, reflecting underdeveloped financial infrastructure.

Rule of Law Concerns: China's political system under the Chinese Communist Party (CCP) lacks independent institutions, transparent legal protections for investors, and checks on government actions—features historically tied to reserve currencies from democracies or republics. Centralized power under Xi Jinping exacerbates this, with no willingness to liberalize fully, as it conflicts with CCP governance.

Network Effects in Global Infrastructure: The USD dominates entrenched global systems due to network effects, where widespread adoption creates self-reinforcing advantages:

Futures markets and refining contracts: Most commodity futures (e.g., oil) and refining agreements remain USD-denominated, requiring dollars for hedging and settlement.

Shipping and insurance: Contracts, bills of lading, and marine insurance are standardized in USD, with switching costs immense due to years of built relationships. Unwinding these would take years or decades, as alternatives lack the scale and trust.

Timeline for Petroyuan Adoption:

Petroyuan adoption—RMB-denominated oil trade—evolves gradually over decades, not months, due to the barriers above. Progress includes RMB surpassing USD in some China-specific metrics by 2024, but global reserve challenges persist without capital account liberalization and political reforms. Sources project no serious USD challenge "any time soon," with full evolution potentially requiring 20-50+ years if reforms occur, or never if CCP control endures; yuan internationalization complements rather than displaces USD.

EXPERT VOICES CONCERNING POSSIBLE SHIFTS:

Petrodollar collapse, Yuan oil trading, and Dollar alternatives oil

Regional banking experts in energy markets and geopolitical strategists view petroyuan adoption as a gradual, limited challenge to the petrodollar rather than an imminent replacement, driven by China's oil demand dominance, sanctions evasion, and bilateral deals but constrained by the dollar's liquidity and yuan's capital controls. Energy Market Perspectives (e.g., akin to Rystad Energy, Energy Aspects). Analysts highlight China's role as the world's top oil importer (15% of global consumption), urging suppliers like Russia, Iran, and Gulf states to accept yuan settlements, fostering bilateral contracts and hedging in yuan. Progress includes Russia, Iran, and Venezuela already using petroyuan, with potential rises from Belt and Road Initiative (BRI) integration and China's alliance with Russia; however, Saudi Arabia and Russia (26% of global oil production) are needed for major shifts, which remain unlikely without them. Check out Oil prices in the last 10 years( 1946-2026) from Macro Trends

A hybrid model is emerging: oil pricing stays in dollars for liquidity, but settlements shift to yuan out of necessity (e.g., during Middle East crises like Hormuz tensions), not preference, creating gradual RMB internationalization without displacing dollar dominance. FX/Geopolitical Strategist Views (e.g., akin to Atlantic Council, CFR) US sanctions on Russia, Iran, Venezuela, and others undermine petrodollar confidence, boosting petroyuan as a sanctions-proof alternative; BRICS efforts and China's CBDC enhance this, but yuan holds <2% of global reserves vs. dollar's 57%.

Structural barriers persist: yuan's limited convertibility, capital controls, opaque markets, and lack of trust hinder full adoption, favoring dollar's safe assets and legal stability.

No rapid overthrow expected; petrodollar endures as reserve currency, with petroyuan coexisting in a multipolar shift, potentially accelerated by geopolitical stress but reversing in some cases (e.g., post-Russia gains).

Overall, experts predict petroyuan growth in niche trade (e.g., Asia, sanctioned nations) over decades, but dollar hegemony persists due to entrenched advantages

LOOKING FORWARD AND ANALYSIS:

Potential investors monitoring the petroyuan's development China's yuan-denominated oil futures trading on the Shanghai International Energy Exchange (INE) should prioritize three key indicators:

Saudi Arabia's Treasury holdings, clearing volume, and Shanghai Oil Futures uptake. These metrics signal de-dollarization progress, international adoption, and liquidity in yuan oil trading, potentially impacting global oil markets and currency shifts.

Saudi Treasury Holdings

Changes in Saudi Arabia's U.S. Treasury holdings reflect its diversification strategy amid petroyuan settlement talks.Declining holdings could indicate shifts toward yuan reserves or petroyuan acceptance, as Saudi Arabia explores non-USD oil sales to China. Rising holdings might signal continued dollar reliance despite BRICS discussions.

Clearing Volume

likely referring to a blockchain or digital asset platform like Ethereum addresses tied to yuan settlements or crypto-oil bridges—clearing volume measures transaction throughput. High or growing volume suggests efficient petroyuan clearing, reducing USD intermediary needs and boosting adoption. Low volume indicates limited use or regulatory hurdles in tokenized oil trades.

Shanghai Oil Futures Uptake

Uptake tracks trading volume, open interest, and foreign participation in INE's Shanghai crude oil futures.Increasing uptake by non-Chinese buyers (e.g., via Hong Kong or overseas brokers) signals petroyuan viability as a dollar alternative.

Key sub-metrics:

delivery volumes (physical yuan settlements) and international investor ratios, confirming liquidity beyond mainland China. Track these alongside broader trading indicators for context: Moving averages (e.g., 50/200-day EMA for futures trends), RSI (overbought/oversold signals above 70/below 30), and MACD (momentum shifts via EMA convergence/divergence). Combine with company metrics like P/E ratios for oil firms and beta for market risk. Rising trends across all three strengthen petroyuan momentum; stagnation or declines highlight dollar dominance.

Check out Oil prices in the last 10 years( 1946-2026) from Macro Trends

HOW A POSSIBLE SHIFT COULD AFFECT PRICES AND LIVELIHOODS:

Oil is priced globally in US dollars (USD), so for consumers in non-USD countries like those using local currencies at a Shell station, importers and retailers must convert USD to the local currency, incurring transaction costs from exchange rate fluctuations, bank fees, hedging, and spreads that get passed along in retail pump prices.

Currency Conversion Costs at Local Fuel Stations:

|

| Photo:Korean Times |

Oil's USD denomination means local prices = global USD oil price × exchange rate (s_t) + conversion costs, per the law of one price: \( o_t = o_t^* - s_t \) (log terms). A weakening local currency raises the USD-equivalent cost of oil imports, adding expenses from forex hedging, brokerage fees, and transaction spreads (e.g., banks charge 0.5-2% on conversions). For oil-importing nations, higher USD oil prices or local depreciation worsens trade balances, further pressuring currencies and amplifying costs at stations like Shell.Retailers mark up to cover these (e.g., 5-10% of price volatility from forex), appearing as higher liter prices.

Shipping Fuel (Bunker Fuel) Effects on Container Rates and Food Prices

Bunker fuel (heavy fuel oil for ships) is priced in USD; rising global oil prices increase bunker costs by 20-50% per barrel spike, directly raising container shipping rates (e.g., $1,000-10,000 per TEU). (Inference: Oil powers 90% of shipping; bunker is ~50% of vessel operating costs, per industry norms.)

Higher container rates (up 10-30% from oil shocks) get passed to importers: transported goods cost more. Food prices rise via this chain—agriculture/processing relies on shipped fertilizers, grains, packaging (e.g., 2022 oil surge added 5-15% to global food freight). (Oil also hits farming fuel/equipment, compounding effects.)

Treasury Demand, 10-Year Yields, and 30-Year Mortgage Rates:

High Treasury demand (e.g., safe-haven buying) lowers 10-year US Treasury yields (supply/demand inverse: more buyers = lower yields/prices). 30-year fixed mortgage rates track 10-year yields closely (~2% spread): lower yields reduce mortgages (e.g., yield drop from 4% to 3.5% cuts mortgages ~0.5%). Oil shocks indirectly tie in—USD depreciation from rising oil boosts commodity prices in local terms, potentially spurring Fed tightening (higher yields). Check out Oil prices in the last 10 years( 1946-2026) from Macro Trends

Are you concerned about dollar strength affecting your savings?

.png)

No comments:

Post a Comment