Is the Transition from the USD to the Chinese Yuan Advisable?

The Petrodollar Under Siege: Iran, the Strait of Hormuz, and the Rise of Yuan Dominance

Published: April 2026 | Category: Global Finance & Geopolitics | Read time: ~7 minutes

|

| Photo:Finnce Feeds |

The USD to Chinese Yuan transition, the petrodollar system, and the de-dollarisation of global trade have become among the most fiercely debated topics in international finance. As geopolitical tensions reshape global alliances, Iran's recent conditions demanding payment in Chinese Yuan — rather than US dollars — for passage through the Strait of Hormuz has reignited urgent questions: Is the global reserve currency shifting away from the US dollar? What would a Yuan-dominated global financial system actually entail? And critically, what are the adverse outcomes of abandoning the US dollar as the world's primary reserve and trade currency? This article examines these questions in depth, arguing that while the Yuan's rise is real, the dollar's dominance remains not just advantageous — but essential — for global financial stability.

KEY TAKEAWAYS

✔ Iran's Strait of Hormuz Yuan demand is a direct, unprecedented attack on the petrodollar system — not a peripheral geopolitical event. |

✔ The Chinese Yuan lacks the open capital markets, transparency, and trust infrastructure that make the USD a reliable global reserve currency. |

✔ A rapid or forced de-dollarisation could trigger inflation, bond market collapse, and deep recession in the United States. |

✔ Yuan dominance would hand China unprecedented geopolitical leverage over global trade pricing, sanctions, and monetary policy. |

✔ The US dollar remains the world's most critical financial stabiliser — its continued dominance is in the global interest. |

✔ Investors, governments, and policymakers should monitor Strait of Hormuz developments as a leading indicator of petrodollar vulnerability. |

The Strait of Hormuz: Iran's Yuan Demand and the Petrodollar's Most Dangerous Moment

|

| Photo:BBC |

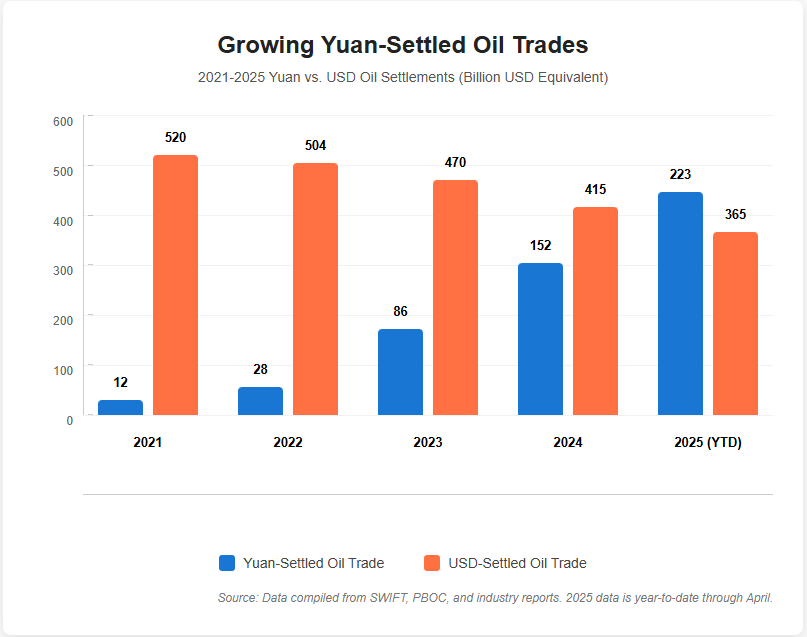

The Strait of Hormuz — through which approximately 20% of the world's oil supply transits daily — has long been a chokepoint of immense strategic significance. However, Iran's stated conditions that nations pay transit-related fees and oil settlements in Chinese Yuan rather than US dollars represents something qualitatively different from past geopolitical posturing. It is a direct structural challenge to the petrodollar system, the 1974 arrangement by which global oil trade is denominated in US dollars, creating a constant international demand for dollars that has underpinned American economic dominance for over five decades.

The implications are significant. If major oil exporters and transit nations begin accepting or demanding Yuan for energy transactions, the foundational logic of the petrodollar begins to erode. The dollar's global demand is structurally tied to oil pricing: nations must hold dollars to purchase oil. Remove that linkage — even partially — and you remove a critical pillar supporting the dollar's reserve status. Iran, already excluded from dollar-based SWIFT systems due to sanctions, has both the motive and the geopolitical alignment with China to push this agenda aggressively. China, for its part, has actively developed the Petro-Yuan through its Shanghai International Energy Exchange (INE) since 2018, laying the technical infrastructure for exactly this kind of transition.

Why the US Dollar Remains the World's Indispensable Currency

Despite growing noise around de-dollarisation, the US dollar's position as the world's reserve currency rests on structural foundations that the Chinese Yuan has not yet — and may not soon — replicate. As of 2025, the dollar accounts for approximately 58–60% of global foreign exchange reserves, and the vast majority of international commodity contracts, cross-border loans, and trade invoices are dollar-denominated.

The dollar's dominance is built on four pillars the Yuan currently lacks: first, deep, liquid capital markets — the US Treasury bond market is the world's largest and most liquid safe-haven asset; second, rule of law and institutional credibility — investors trust that dollar-denominated assets will not be arbitrarily seized or devalued by political decree; third, full currency convertibility — unlike the Yuan, which operates under strict capital controls, the dollar flows freely across borders; and fourth, network effects — the dollar is entrenched in global invoicing, derivatives, and correspondent banking in ways that create enormous switching costs.

These are not minor advantages. They represent decades of institutional trust-building that China's financial system, for all its growth, has not yet matched. The Yuan's share of global reserve holdings remains below 3%, a figure that starkly underscores the gap between geopolitical ambition and financial reality.

What a Chinese Yuan-Dominated Global Financial System Would Actually Entail

Should the Chinese Yuan replace the US dollar as the dominant global reserve currency, the transition would be neither smooth nor benign. It would represent the most significant restructuring of the global monetary order since the Bretton Woods system. Here is what such a transition would likely involve:

Restructuring of global trade invoicing: Commodities — oil, gas, metals, agricultural products — would increasingly be priced and settled in Yuan, requiring nations to accumulate Yuan reserves. This is already occurring in bilateral China-Russia, China-Saudi Arabia, and China-Iran energy deals.

Shift of financial gravity to Chinese markets: Beijing's bond and equity markets would become the global safe-haven of choice, giving China enormous influence over global interest rates, capital flows, and credit conditions — power currently wielded by the US Federal Reserve.

Geopolitical leverage through monetary policy: China would gain the ability to impose its own version of dollar-style financial sanctions, controlling access to the Yuan payment system (CIPS) as a geopolitical weapon — precisely the kind of leverage it currently criticises the US for wielding through SWIFT.

Capital account liberalisation pressure: For the Yuan to function as a true reserve currency, China would eventually need to open its capital account, creating domestic financial risks Beijing has so far been unwilling to accept, including vulnerability to capital flight and speculative attacks.

The Most Adverse Outcomes: What Dollar Decline Would Mean for the United States and the World

|

| Photo: Reuters |

The adverse outcomes of dollar displacement are not hypothetical abstractions — they are economically quantifiable catastrophes. For the United States, the most severe scenario of rapid de-dollarisation would trigger a cascade of crises:

Loss of exorbitant privilege and rising borrowing costs: The US currently borrows at low rates because global demand for Treasuries is structurally inflated by dollar reserve status. If that demand collapses, US Treasury yields would spike dramatically, forcing brutal cuts to government spending or triggering a sovereign debt crisis — a phenomenon the US has never experienced.

Imported inflation: A weakened dollar means more expensive imports across the board — consumer goods, electronics, pharmaceuticals, and critically, energy. American households would face a sustained cost-of-living shock of a magnitude not seen since the 1970s stagflation, compounded by the loss of the commodity pricing advantage the petrodollar provides.

Collapse of US financial sector dominance: Wall Street's centrality in global finance — from IPOs to bond issuance to derivatives — is predicated on dollar primacy. Dollar displacement would fundamentally disrupt the business model of US financial institutions and erode New York's status as the world's premier financial centre.

Erosion of US geopolitical power: Dollar-based sanctions — America's most powerful non-military foreign policy tool — would become substantially less effective as more trade migrates to Yuan-settled systems. This would constrain US foreign policy options at precisely the moment when geopolitical competition with China is most intense.

For the global economy, the transition risks would be equally severe. The fragmentation of global finance into dollar and Yuan blocs would raise transaction costs, reduce capital efficiency, and introduce a new axis of systemic financial risk. Emerging market economies that have borrowed in dollars would face devastating mismatches if the dollar strengthens sharply during a disorderly transition.

Why Dollar Dominance Must Be Defended: The Case for Keeping the USD at the Centre

The argument for maintaining US dollar dominance is not merely one of American self-interest — it is one of global financial stability. The dollar's reserve status underpins the architecture of international finance: trade finance, correspondent banking, sovereign debt markets, and commodity pricing all function with the dollar as the common denominator. Replacing that common denominator with a currency controlled by a single-party state with opaque monetary policymaking, capital controls, and a track record of strategic currency management would not be progress — it would be regress.

The United States must respond to the Strait of Hormuz challenge and Iran's Yuan conditions not merely with sanctions or military posturing, but with a coherent monetary strategy: reinforcing dollar-based energy diplomacy, deepening financial ties with Gulf states, and working with allies to ensure that oil pricing remains anchored in dollars. Simultaneously, the US must address the domestic fiscal credibility concerns — chronic deficits and debt ceiling brinkmanship — that give ammunition to those arguing the dollar is an unreliable reserve anchor.

The Yuan's rise as a trade currency is a reality that cannot be wished away. But a managed, rules-based international monetary system with the dollar at its core remains overwhelmingly preferable to one reorganised around Beijing's financial interests and political imperatives.

Resources for Further Reading

1. International Monetary Fund (IMF) — Currency Composition of Official Foreign Exchange Reserves (COFER): https://data.imf.org — Quarterly data on global reserve currency shares; essential for tracking dollar vs. Yuan reserve trends.

2. Bank for International Settlements (BIS) — Triennial Central Bank Survey: https://www.bis.org/statistics/rpfx22.htm — The definitive global survey of foreign exchange market turnover and currency usage in international finance.

3. Council on Foreign Relations — The Dollar and US Power: https://www.cfr.org — In-depth policy analysis on the geopolitics of dollar dominance and de-dollarisation pressures.

4. Peterson Institute for International Economics (PIIE): https://www.piie.com — Leading economic research on currency competition, petrodollar dynamics, and the renminbi's international role.

5. US Energy Information Administration (EIA) — Strait of Hormuz Factsheet: https://www.eia.gov — Data and analysis on oil flows through the Strait of Hormuz and their significance for global energy markets.

The dollar debate is not over — it is just beginning. Share this article to inform the conversation.

Tags: US dollar dominance | Chinese Yuan reserve currency | petrodollar | de-dollarisation | Strait of Hormuz | USD vs Yuan | global reserve currency | currency transition risks

.png)

No comments:

Post a Comment